By Emeka Anaeto, Economy Editor

AMID impressive third quarter results investors have sustained bullish positions on the stocks of Guaranty Trust Bank Plc, GTB, and that of Zenith Bank Plc.

Though stock dealers expect further uptick up till end of this week they also foresee profit taking by next week.

The impressive results were coming amid domestic macroeconomic headwinds that have pressured economic activities during the period, while undermining most of the operators in the banking sector.

The two banks have been the toast of the markets in terms of brand equity and actual financial performance in the past decade. They are traditional rivals.

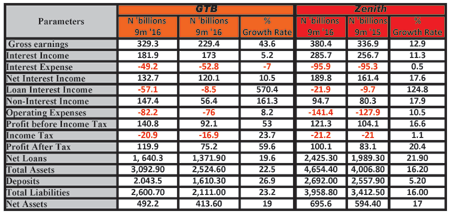

Topline: GTB leads growth rate, Zenith leads volume

GTB’s gross earnings expanded 43.6 per cent year-on-year, YoY to N329.3 billion from N229.4 billion in 2015 principally due to the 5.2 per cent YoY growth in interest income and massive 161.2 per cent YoY expansion in non-interest income. The growth in interest income was driven by 15.2 per cent rise in interest from loans and advances, which accounted for 77.3 per cent of total interest income.

YoY Zenith’s gross earnings at N380.4 represented a modest 12.9 per cent growth, driven by equally modest 11.3 per cent growth (significantly higher than GTB’s 5.2%) in interest income. Non-interest income, at N94.7 billion in Zenith, represented a modest 17.9 per cent uptick, as compared to the massive jump recorded by GTB on this income line.

Deposit growth, Cost of Funds

Remarkably, GTB was able to attract deposits at significantly lower cost while growing its deposit base significantly by 26.9 per cent to over N2.0 trillion. Interest expense declined by 7.0 per cent thus moderating annualized Cost of Fund (CoF) to 3.0 per cent from 3.1 per cent in the first half of 2016, H1’2016.

Consequently, Net Interest Income rose 10.5% while Net Margin improved to 36.4 per cent.

In Zenith, the numbers showed growth rate in customer deposit slower at 5.2 per cent to N2.7 trillion with cost in terms of interest expense coming higher at 0.5 per cent increasing to N95.9 billion.

However, Zenith’s Net Interest Income growth rate came significantly better at 17.6 per cent to N189.8 billion but Net Margin settled (below GTB’s) at 26.3 per cent.

Impact of Foreign Exchange gains

Notably, GTB’s massive 161 per cent growth in Non-interest income came on the back of the bank’s huge N93.6 billion recorded in foreign exchange revaluation gains, which shows a N32.3 billion increase from H1’16 (52.6% QoQ) as the Naira depreciated further in third quarter, Q3’16 (-10% QoQ).

Similarly, at Zenith, though growth rate in this income line came less at 18 per cent its Non-interest income was also on the back of the bank’s foreign exchange revaluation gains, but which, compared to GTB’s, also came less in quantum at N28 billion in Q3’16. Very importantly, in Zenith the foreign exchange revaluation gains obliterated the adverse impact of the 15 per cent decline it recorded on Fees and Commission income line, most likely as a result of the suspension of Commission on Turnover (COT).

Bad loans bad for all

As if everything had to come massive at GTB, the impairment charges for bad loans trended massively higher during the third quarter, growing by 570 per cent, one of the worst in the industry, to N57.1 billion.

With the numbers recorded by GTB on impairment charges it appeared Zenith’s figures, which ordinarily should be alarming, now looks ‘good’ growing by 124.8 per cent, though remained relatively flat quarter-on-quarter, QoQ.

Bad loans have been bad for almost all banks since 2015 and have worsened in 2016 with Central Bank of Nigeria’s recent reports sounding very alarming on this performance indicator.

Disclaimer

Comments expressed here do not reflect the opinions of Vanguard newspapers or any employee thereof.