As highest lending rate tends to 50%

Analysts defend banks’ position

By Babajide Komolafe

ALMOST one year after the Central Bank of Nigeria, CBN, began a drive towards lower interest rates, about eighteen banks have declined to toe the apex bank’s policy line.

In the fourth quarter of 2017, the CBN had begun the process of influencing interest rates downward, dropping rate of its key monetary instrument, the Nigerian Treasury Bills, NTB, which fell by 284 basis points (bpts) between December 2017 and April this year, a move targeted at forcing the banks to pull back their stockpile of funds in the instrument, thereby pushing up banking system liquidity in favour of lending to the private sector as well as lowering their rates.

Financial Vanguard analysis revealed that interest rate on TBs has been trending downward since mid last year. From 16.5 percent in July 2017, average interest rate on fresh (primary market) TBs fell by 200 bpts to 14.6 percent in December, 2017. From December average interest rate on NTBs fell further by 284 bpts to 11.66 percent in April this year.

CBN Headquarters

Movement in banks’ interest rate

But Financial Vanguard investigations have revealed that only seven banks responded in this targeted direction by reducing their lending rates, while in addition to the 17 than remained at high point interest rate, one bank actually increased its lending. Some of the banks, however, defended their lending rates citing various factors including the Monetary Policy Rate (MPR) which has been at 14 percent since second quarter of 2016, the Cash Reserve Ratio (CRR) which is 22 percent and risk profile of the borrowers.

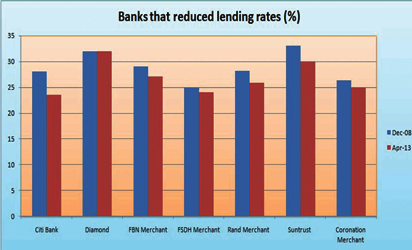

Financial Vanguard analysis of the highest lending rates charged by banks as published by the CBN, showed that during this period the seven banks that reduced their highest lending rates are Citi Bank, Coronation Merchant Bank, Diamond Bank, FBN Merchant Bank, FSDH Merchant Bank, Rand Merchant Bank and Suntrust Bank. On the average the highest lending rates charged by the seven banks fell by 162 bpts between December 8, 2017 and April 13, 2018. Also, the spread between the average deposit rate and highest lending rate of the banks fell on the average by 192 bpts. All the seven banks, with the exception of Diamond Bank, recorded decline in spread between the average deposit rate and highest lending rate during the period.

Further analysis revealed that the highest lending rate charged by Citi Bank fell to 23.5 percent as at April 13, from 28 percent on December 8, 2017, while the spread between the average deposit rate and highest lending rate fell by 700 bpts. For Coronation Merchant Bank, the highest lending rate fell to 25 percent from 26.3 percent, while the spread fell by 54 bpts. For Diamond Bank the highest lending rate fell slightly to 31.91 percent from 31.98 percent, while the spread rose by 25 bpts.

For FBN Merchant Bank, the highest lending rate fell to 27 percent from 28.95 percent, while the spread fell by 45 bpts. For FSDH Merchant Bank, highest lending rate fell to 24 percent from 25 percent while the spread fell by 95 bpts.

Highest lending rate

For Rand Merchant Bank, the highest lending rate fell to 25.77 percent from 28.13 percent while the spread fell 146 bpts; while for Suntrust Bank, the highest lending rate fell to 30 percent from 33 percent while the spread fell by 330 bpts.

According to the CBN data, the 17 banks left their highest lending rates unchanged. The banks and their highest lending rates are: Access Bank (30.25 percent), Ecobank (30 percent), First Bank (30 percent) FCMB (30 percent), Fidelity Bank (40 percent), GTBank (26 percent), Heritage Bank (33 percent), Keystone Bank (34 percent), Providus (25 percent), Standard Chartered Bank (27 percent), Skye Bank (36 percent), Stanbic IBTC (36 percent), Sterling Bank (33 percent), UBA (29 percent), Unity Bank (32 percent), Wema Bank (31 percent) and Zenith Bank (34.5 percent).

Union Bank, however bucked the trend by raising its highest lending rate during this period. According to the CBN, Union Bank, raised its highest lending rate to 49.05 percent from 42 percent, while the spread widened by 949 bpts.

Banks with highest lending rates

According to the CBN, as at April 13, Union Bank charged the highest maximum lending rate of 49.05 percent, which applies to the sector categorised as ‘General’. Fidelity Bank followed with 40 percent, which applies to sectors categorised as ‘General Commerce’ and ‘General’. Stanbic IBTC and Skye Bank followed with 36 percent applied to sectors categorised as Agriculture, Manufacturing, Information Technology, General, Extra Territorial and General Commerce sectors.

Banks’ Response

While, some of the banks did not respond to Financial Vanguard enquires, Union Bank, Skye Bank, and Fidelity Bank explained the factors responsible for their high lending rates.

Defending Union Bank’s decision to raise its lending rate, Head of Corporate Affairs and Corporate Communications, Ogochukwu Ekezie-Ekaidem said: “In addition to macro-economic factors, there are several factors which determine a bank’s lending rates per time including the cost of processing the loans, operational costs and cost-to-income ratio; all of which are bank-specific.

“These factors hold sway even with changes in Treasury Bill rates and our lending rates are set after all of these are considered. The lending rates for small and personal loans are fixed on a case-by-case basis, depending on factors such as customer’s income and risk profile.

At Union Bank, unlike many other banks, we offer small loans to customers outside the traditional salaried segment; for example self-employed individuals, who often do not have this access to financing. Because these segments have a higher risk profile, it tends to make lending rates to them higher.”

Skye Bank on its part explained that the 36 percent lending rate is imposed on customers who defaulted on the loan repayment obligations. The bank in a statement said: “The lending rate of 36 percent quoted is the penal rate for customers that have defaulted on their obligations. This is to reflect the CBN allowable 1.0 percent flat per month penal rate for defaulting customers over and above the contractual rate.

“Our lending rate is tied to the Monetary Policy Rate (MPR) as directed by the CBN, and downward review of contractual rates will not be obvious until MPR is reduced. The maximum lending rate is also tied to customers’ segments to reflect associated costs and risk premium. The anchor rate for lending in the industry is MPR as guided by the CBN. Just to emphasize.”

On his part, Gbolahan Joshua, Chief Operations and Information Officer (COIO), Fidelity Bank Plc, said that the 40 percent highest lending rate charged by the bank is based on risk attached to the least rated borrower. “We adopt a risk based pricing methodology and the rate above is based on the level of risk the bank has taken for the least rated obligors on its books,” he said.

On why the bank has not lowered its highest lending rate, he stated: “Lending rates are based on the risk profile of customers and the highest or lowest lending rate does not tell the real story of the trend of lending rates for a bank.

“If you look at our Q1’18 numbers you will see that our average yield on loans declined from 16.5 percent in Q4’ 17 to 15.6 percent showing that our lending rates have come down by over 90bps. Our average lending rates have declined by over 0.9 percent or 90bps from 16.5 percent in Q4’17 to 15.6 percent in Q1’18.”

Analysts’ comments

Explaining why most banks have not adjusted their lending rates downward, Olusegun Alebiosu, Chief Risk Officer, First Bank stated: “Lending rates remain high for a number of reasons. Savings interest rate is mapped to Monetary Policy Rate (MPR) and MPR is yet to change. It is also important to note that cash reserve requirement (CRR) is 22 percent. That has a lot of implications for interest rate. That is yet to change. If we still have these two conditions in place, interest rate cannot come down the way they envisage.”

Commenting on the disparity in the movements of banks’ lending rates in relation to falling yields on government securities, Ayo Akinwunmi, Head of Research, FSDH Merchant Bank said: “A lot of lending in Nigeria is done on different indicators. Certain lendings are predicated on MPR. Now MPR has remained the same for a very long time. So if they say MPR plus four is the lending rate we are going to charge, what that means then is that the lending rate will remain the same situation not minding the fact that fixed income securities have come down.

Fixed income securities

“Now some transactions are based on Nigeria Interbank Offered Rate (NIBOR). Now NIBOR sometimes moves in line with liquidity in the market or yields on fixed income securities.

“So if the yield on fixed income securities or the NIBOR in the market come down, which I think, it may have come down, it means the lending rate for that period will go down.

“Although in between the periods there could be spikes. There could be some periods that there is huge liquidity deficit, maybe CBN debits some money from the system and the market is tight, there could be some time when the NIBOR rate could went as high as 70 percent, 80 percent, sometimes reaching 200 percent. And unfortunately, if any money matures during that period, that would be re-priced during that period, it would take into consideration that spike, then it would influenced the lending rates they quote upwards.

“So those are just the various things, but people will say why is lending rate coming down because the yield is coming down. There could be, and it may not necessarily be, there could be some lending predicated on the yields on government securities in the market. So they may say whatever Treasury bill is doing we are going to do four percent above it. So those are various factors that may lead to those issues.”

Disclaimer

Comments expressed here do not reflect the opinions of Vanguard newspapers or any employee thereof.