By Obadiah Mailafia

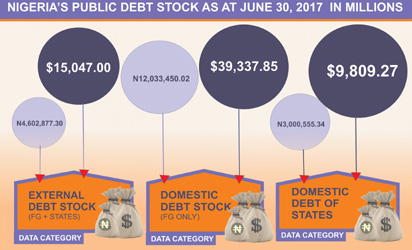

THE latest statistics on the national debt indicate that we owe some US$15.05 billion to foreign creditors and a staggering N14.06 trillion to domestic creditors.

The recently announced N100 billion sukuk bond with a maturity of 7 years at 9.0% interest comes as an addition to the national growing debt. Let me make it clear that I have nothing against the sukuk bond. In a globalised world economy with growing and diversified financial markets, financial products and services should be structured for all who need them. Same goes for sukuk, which is demanded by Muslim investors.

I do not know what became of the proposed request submitted by Federal Government to the National Assembly last year on the plan to borrow the sum of US$29. 960 billion under the external borrowing plan for the years 2017-2020.

I am keenly aware that our financing needs, especially in the infrastructure sector, are considerable. There is no disputing that. What we demand is caution and greater due diligence in committing our country and future generations down that old, discredited route.

Lest we forget, it was barely ten years ago, precisely in the year 2006, that our country threw off the shackles of debt peonage in settling our external debt obligations with the Paris Club of international creditors. It was a very painful surgery and very costly in terms of our financial obligations.

But it was a necessary surgery. Before then our external debts had amounted to US$36 billion, most of them accruals from interest obligations. It was difficult for the fiscal policy space because we had to pay an average of US$5 billion annually in interest payments alone, not to talk of the principal. With that trend, it would have taken another half-century to pay off our total debts.

Contrary to what some have suggested, settling the debt with the Paris Club at the time we did was certainly the right thing to do. Before then, we were de facto slaves of the international financial agencies. After that settlement, we had the breathing space to rebuild the foundations of our common prosperity. I have been told that many of the Western powers bit their fingers in frustration that a big fish such as Nigeria was let off the hook of their control with such ease.

Unfortunately, like the Bourbon kings of eighteenth century France, we seem to have learned nothing and forgotten nothing. We seem hell-bent on plunging, headlong and blindfolded, into the bottomless dungeon that, only a few years ago, we had been taken out of. I am not saying we cannot borrow from abroad. To do so, we need fulfil a number of critical conditions.

First, I will insist that no single dollar from outside should be borrowed for social and human capital programmes such as education and health. We can construct the buildings needed with local funds. We need to build our own medical technology and produce medicines locally instead of borrowing to import those inputs.

During our tragic civil war in the years 1967-1970, Nigeria did not borrow a single dollar to finance the war effort. During the post-war reconstruction, we also did not need to borrow money from anybody. The late sage, Chief Obafemi Awolowo of blessed memory, was Finance Minister of the time. He handled our public finances with such consummate skill and ability that we did not have to borrow either for the war or for reconstruction. Why must we do it today? Why?

Secondly, I would insist that we must engage in external borrowing only for infrastructure projects. And even on that, not just all infrastructures. We should borrow externally only for infrastructures that demonstrably can pay their way in terms of economic and financial returns on investments. Examples of these are power and electricity, railways, harbours and ports, mass transit systems, water supply and the rest of it.

Thirdly, there is need for government to explain to us very clearly the terms of repayment and the conditionalities attached to the proposed loans. We know that international agencies such as the World Bank still impose rather onerous conditionalities as do their multilateral regional counterparts. As Nigeria is considered a ‘blend country’ by those agencies (i.e. a mix of low-income as well as middle-income status), we have the privilege of borrowing at reduced terms.

We also have access to soft financing as provided by the International Development Association, an affiliate of the WB and the African Development Fund, ADF, the soft-loan window of the African Development Bank Group. Finally, it is important that we review the implications for the proposed external borrowing in terms of our overall external and total debt position. As I understand it, our total debt – external and internal – has already reached the US$36 billion level. This is precisely the total amount that we owed external creditors when we went into the Paris negotiations in 2006.

What is different today is that the naira denominated debt is far higher than our dollar denominated debt obligations, which currently stand at US$15.05 billion. Should we go ahead to borrow an additional US$29.960 billion, our total external debt would rise to a whopping US$45 billion. At present, our debt to GDP ratio stands at 12.77 percent. If we go ahead with borrowing plan, the debt to GDP ratio would have risen to 19 percent. Some would argue that this would still not be that bad, especially given that the average expected for emerging market economies like ours is a debt to GDP ratio of 40 percent.

Honestly, we need to be sceptical about this argument about debt to GDP ratio. Why do I say so? It is simply because, even as we speak, we are already committing an average of 30 percent of our annual budget to debt repayment. It is estimated that 66% of government revenues currently go to servicing debt. If the magnitude of debt increases, it would simply dig deeper into our annual budget.

Countries with a high debt to GDP ratio such as Malaysia, Indonesia and Brazil are well diversified economies that have multiple income streams from international trade. We still find ourselves in a situation where oil accounts for over 70 percent of revenues and 95 percent of our foreign earnings. In our own case, therefore, we need to go softly on external borrowing, because we simply have no margin of safety as far as foreign earnings are concerned.

Judgement and prudence demand that we tread cautiously while applying rigorous and exacting criteria for external as well as internal borrowing going forward.

Disclaimer

Comments expressed here do not reflect the opinions of Vanguard newspapers or any employee thereof.