…Sees 192% spike in synthetic document fraud

… Banks, Fintech, Consulting services bear brunt

By Juliet Umeh

Despite a new data revealing sharp decline in traditional identity scams in Nigeria, the country is still suffering from an alarming dimension of identity fraud in almost all aspects of her economy. The economy is witnessing a surge in synthetic identity fraud, especially in the financial sector.

Synthetic identity fraud is a type of financial crime where fraudsters create a completely fake identity by combining real and fake information.

Unlike traditional identity theft where a criminal steals and uses someone else’s existing identity, synthetic identity fraud involves building a new identity that doesn’t belong to a real person.

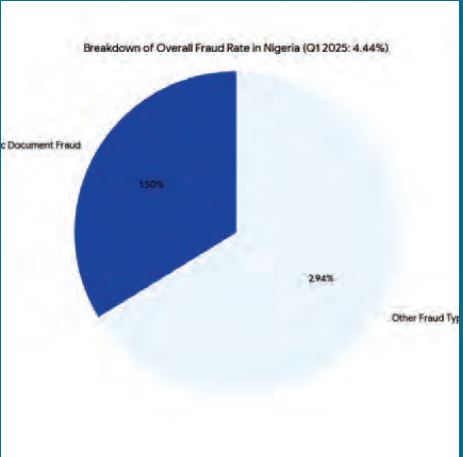

Global verification company, Sumsub, in its first quarter, Q1 2025 report finds that the overall fraud rate in Nigeria rose to 4.44 percent, up 2.5 percent year-on-year, despite a dramatic 80 percent drop in document forgery fraud, a traditional method long used by scammers.

While this may appear to be good news on the surface, experts warn it signals a deeper shift in criminal tactics.

Sumsub’s VP of Sales for Africa, Hannes Bezuidenhout said: “Enhanced verification tools have decimated traditional document forgery, but criminals are adapting with synthetic IDs and AI-powered scams. The data proves that fraud prevention is now a race between innovation and adaptation.”

Synthetic fraud on the rise

Synthetic identity fraud, a more advanced form of scam involving the use of fictitious or AI-generated documents, is now gaining ground in Nigeria.

Sumsub reports a staggering 192 percent increase in synthetic document fraud within the country, accounting for over 1.5 percent of all verification attempts.

This places Nigeria among the most affected African nations, trailing only Tanzania, where synthetic fraud has crossed 2 percent, and South Africa, where the synthetic attack rate remains low but its growth rate soared by 480 percent.

Document forgery collapsing across Africa

Across the continent, traditional document forgery has plummeted, declining by 82 percent year-on-year from 0.51 percent to 0.09 percent. Nigeria’s own 80 percent drop contributes significantly to this trend. South Africa recorded a 73 percent fall, and Ghana nearly 50 percent.

Industry impact: Financial sectors most at risk

In Nigeria and across Africa, industries most affected by the new wave of identity fraud include:

Traditional Finance: 3.22% fraud rate (+35% YoY)

Fintech: 3.16% (+7.1% YoY)

Crypto: 4.18% (+2% YoY)

Professional & consulting services: 5.66% (+11.2% YoY)

Meanwhile, areas like gaming, IT services, and online dating are seeing much less fraud. This is because they have made their security checks a lot better.

However, experts warn that no sector is immune. Bezuidenhout said: “Financial institutions must urgently prioritise digital identity threats,”

Regional picture

While South Africa appears to be leading in fraud reduction with a 26.2 percent drop in overall fraud, countries like Tanzania (+9.6%) and Ghana (+10%) recorded sharp increases in fraud rates, despite making gains against document forgery.

Kenya stands out positively, reporting a 15.5 percent reduction in overall fraud and a 45 percent decrease in document forgery.

The road ahead for Nigeria

As criminals turn to AI and synthetic techniques to outsmart verification systems, experts suggest that the only viable defense lies in digital innovation. Businesses in Nigeria must adopt robust, AI-aware identity verification solutions to stay ahead of emerging threats.

Bezuidenhouta advised: “The fraud battle has evolved beyond paper. Nigeria must now win it in the digital arena. “

How it generally works

*Gathering real information: The fraudster obtains a piece of real, legitimate personal information, most commonly a Social Security Number (SSN) (or its equivalent in other countries). These SSNs are often stolen from data breaches, the dark web, or by targeting individuals unlikely to monitor their credit, like children or the elderly.

*Creating the fake identity: This real piece of information is then combined with made-up details like a false name, a fictitious date of birth, an invented address, and a fake phone number. This combination creates what’s sometimes called a “Frankenstein ID.”

*Building credibility (the “sleeper” phase): The fraudster then uses this synthetic identity to apply for small lines of credit (like a store credit card). Initially, these applications might be rejected due to a lack of credit history. However, each application helps create a credit file for the synthetic identity. The fraudster then patiently cultivates this identity by making small purchases and consistently making on-time payments. Over months or even years, this builds a positive credit history and higher credit limits for the fake identity.

*The “bust-out”: Once the synthetic identity has established good credit and access to significant funds, the fraudster “busts out.” This means they max out all available credit lines, take out large loans, or make high-value purchases, and then disappear without any intention of repaying the debt. Since the identity isn’t linked to a real person, it’s very difficult to track the fraudster down.

Why it is hard to detect

*No clear victim: Unlike traditional identity theft where a person realizes their identity has been stolen, with synthetic fraud, there’s often no “real” person to report the crime. The primary victims are the financial institutions or businesses that extend credit.

*Looks legitimate: Because it blends real and fake data, and often has a cultivated credit history, synthetic identities can easily pass traditional fraud detection systems.

*Long-term play: The time fraudsters spend building the identity makes it seem more credible and harder to flag as fraudulent.

*Difficult to trace: Without a real person to trace, law enforcement faces significant challenges in identifying and prosecuting these criminals

Disclaimer

Comments expressed here do not reflect the opinions of Vanguard newspapers or any employee thereof.