By Biodun Busari

Nigeria’s two major problems are security challenges and poor economy. While almost every part of the country is unsafe, inflation bites hard as prices of food keep soaring.

Nigeria’s inflation rate in the month of June 2022, skyrocketed to 18.6% as the people are yet to recover from 17.71% recorded in May.

This is according to the recently released consumer price index (CPI) report for the month of June 2022, by the National Bureau of Statistics (NBS).

Read Also: FG deficit to hit 6.1 % of GDP – IMF

This pathetic state of the nation’s economy is actually one of the reasons Nigerians are agitated as to who becomes the next President to succeed Muhammadu Buhari in 2023.

The three major frontliners positioned to be Africa’s most populous country’s leader next year are Bola Tinubu of the All Progressives Congress (APC), Atiku Abubakar of the Peoples Democratic Party (PDP) and Peter Obi of the Labour Party (LP).

The trio hinted on what they plan in reviving the economy to make it better than its current condition. The question is, if elected President, can any of them revitalise the Nigerian economy to be a prosperous haven for its people, again as it was experienced in 2002?

GDP of record

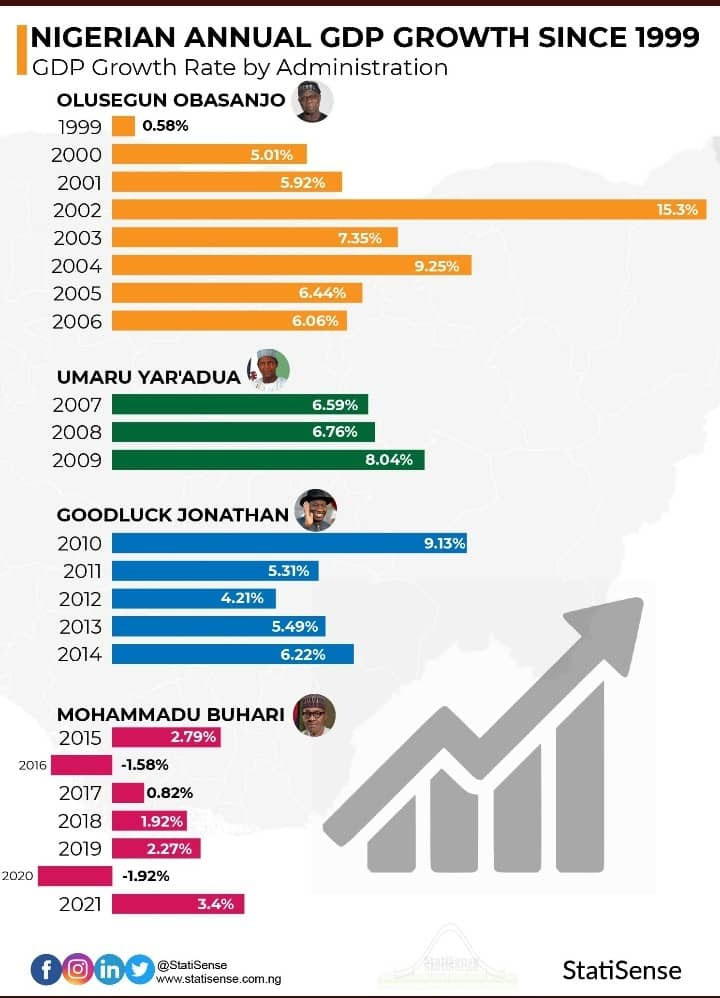

According to data from Nairalytics, under former President Olusegun Obasanjo, Nigeria’s first democratically elected President since the return to democracy in 1999, the economy grew by just 0.58% in his first year of presidency, but recorded its highest rate of 15.33% in 2002.

Be that as it may, according to Statisense, the best annual Gross Domestic Product (GDP) growth rate Nigeria had since 1999 was 20 years ago which was during the Obasanjo’s administration with 15.3%.

In Buhari’s government, the annual GDP growth rate in 2021 was 3.4% which was the best since the retired army general took over the affairs of the country in 2015. The worst under his government was –1.92% in the 2020, the coronavirus-laden year.

For the records, Nigeria had the best GDP growth rate of 8.04% under the former President Umaru Yar’Adua in 2009, while the best under former President Goodluck Jonathan was in 2010, which was 9.13%.

Examining what was responsible for the GDP growth in 2002, exactly 20 years ago, the Nigerian economy advanced under Obasanjo’s presidency due to private sector reforms in telecommunication, banking, and pension administration among other sectors.

The three musketeers’ promises

While it is believed in some quarters that Atiku, as the vice-president under Obasanjo, could not take credit for the economic feat, the PDP presidential candidate has boasted umpteenth times that he could take Nigeria back to the good old days.

In May, speaking on his proposed projects to resuscitate the nation’s economy if elected President, Atiku said he would “reaffirm the critical nature of private-sector leadership and greater private sector participation in development; while repositioning the public sector to focus on its core responsibility of facilitation and enabling the appropriate legal and regulatory framework for rapid economic and social development.”

He promised to “break government monopoly in all infrastructure sectors, including the refineries, rail transportation and power transmission and give private investors a larger role in funding and managing the sectors, thus emulating the benefits accrued in the oil and gas and telecom sectors.”

His colleague from APC, Tinubu, politically popular for laying the foundation of economic reforms of Lagos since 1999, vowed that Nigeria would be a robust economy under his watch if the Nigerian people make him President in 2023.

Tinubu said that Nigeria will become “a country with a vibrant economy, where prosperity is broadly shared by all irrespective of class, region and religion; a nation where its people enjoy all the basic needs.”

In proffering solutions to end Nigeria’s economic woes if voted the country’s President, Obi, the former Anambra governor and a self-made billionaire, said Nigeria will become a productive country. He talked about removal of subsidy and tourism as one of the ways of growing economy.

“The consequence of borrowing for consumption today is that Nigeria is spending over 90 per cent of its revenue to service debts without much production to show for it.

“Exporting crude oil has not saved Venezuela or any country. We need to invest in our massive landmass and grow our economy like other nations such as Singapore, Vietnam and even Morocco have done with tourism,” Obi said.

Disclaimer

Comments expressed here do not reflect the opinions of Vanguard newspapers or any employee thereof.