Nigerian banks have improved non-performing loans (NPLs) post-recession. However, our study shows certain sector NPLs have deteriorated. Real Estate, a significant component of GDP, has also recorded impressive moderation in NPLs, notwithstanding its declining contribution to GDP.

FX

So far in September, the CBN’s gross foreign exchange reserves has shed US$1.19 billion, 2.75% of its value to US$42.16 billion. Foreign Portfolio Investment (FPI) flows into the country has significantly fallen. For Q3 2019, FPI flows fell by 50.30% q/q to US$2.04 billion, accounting for just 26.71% of inflows (compared with Q2 FPI flows which accounted for 61.31% of FX inflows). With the fragile state of the global economy, investors are increasingly picky with what countries attract their investments.

Bonds & T-bills

The yield on a Federal Government of Nigeria (FGN) Naira bond with 10 years to maturity rose by 1bps to 14.39%, and at 3 years rose by 14bps to 14.27% last week. The yield on a 364-day T-bill rose by 5bps to 15.15%. The yield on a T-bill with 3 months to maturity rose by 53bps to 12.70%.

Our oft-stated view that one-year risk-free Naira-denominated rates need to trade 250-300bps above inflation is now challenged as rates are trending at 413bps above August’s inflation print of 11.03%. This positions Naira-fixed income assets favourably relative to other emerging markets.

Oil

The price of Brent fell by 3.69% last week to US$61.91/bbl. The average price, year-to-date, is US$64.81/bbl, 9.60% lower than the average of US$71.69/bbl in 2018, but 18.38% higher than the US$54.75/bbl average seen in 2017.

Brent crude saw its biggest weekly decline in the month of September last week on the back of easing tensions in the Middle East; and positive developments in the US/China trade war. Following the United Nations (UN) climate change summit in New York last week, about 130 international banks have signed the Principles for Responsible Banking, which entails their commitment to fully supporting the implementation of the Paris Agreement, by decreasing hydrocarbon investments while promoting renewables. While the world is still some odd decades away from reduced reliance on oil, the threat this poses should not be ignored, especially for an oil-dependent nation like Nigeria.

Equities

The Nigerian Stock Exchange (NSE) All-Share Index fell by 0.09% last week, pushing the year-to-date return to negative 11.95%. Last week Seplat (+21.00%), Nestle Nigeria (+11.15%) and Lafarge Africa (+5.96%) closed positive while STANBIC IBTC (-11.32%), CCNN (-9.94%) and Presco (-9.93%) fell.

The NSE, last week, recorded only two positive trading sessions out of five as sell pressures persisted in the market. With little to no improvement in investor sentiment, we see trading activity in the equity space being tepid. We reiterate our view that select stocks are trading at historical lows and might pose as good entry points for strategic investors.

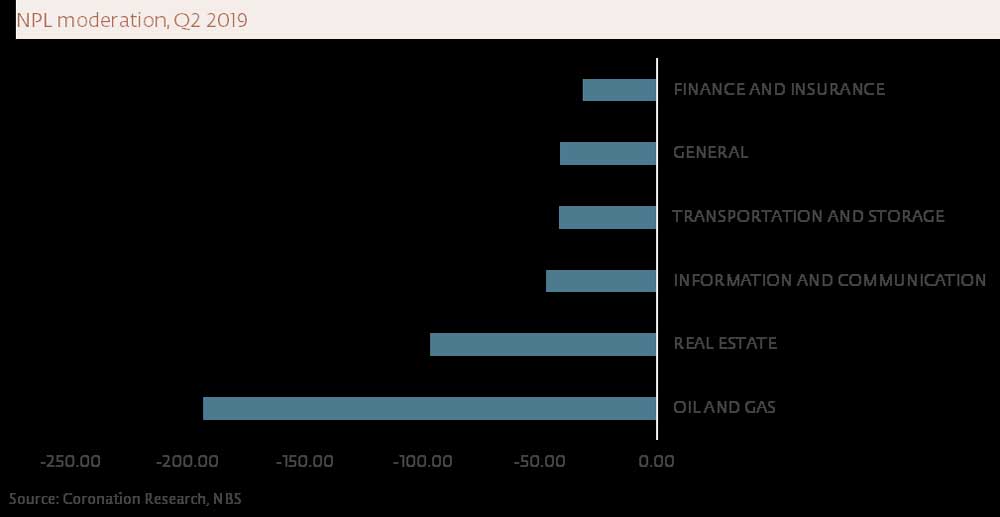

A better NPL picture

Post recession, banks have taken prudential actions together with restructuring to pare the level of non-performing loans (NPLs) in the industry. The tier-one banks achieved this without suspending dividend payments to shareholders. Recently, some of the tier-two banks have announced recoveries against their NPL levels to further improve the industry outlook.

However, NPL’s in the Power and Energy sector have deteriorated. NPL’s rose by 34.83% y/y in Q2 2019. This state of affairs in the Power and Energy industry stands at variance with the rest of the private sector as it remains the only private sector segment with deteriorating NPL as at Q2 2019.

Moderation of NPLs from the Oil and Gas sector was 193bn, the largest nominal change recorded y/y and more than 2x the level of moderation in the Real estate sector, the second largest source of NPLs. Communications completes the top three sectors with the largest NPLs.

While we can point to improving oil production to corroborate the improvement in NPLs in the Oil and Gas sector, the development in the Real Estate segment is less clear. For one, the share of Real Estate as a component of GDP has been declining. Also, in 10 of the last 11 quarters Real Estate posted negative growth rates and occupancy rates have not improved significantly. Finally, the stock of credit to the sector is only 78% of its size in Q2 2018, which is the most severe contraction across all segments.

Coronation Weekly Update

There is however some positive news. An increasing number of residential Real Estate managers are creating more flexible structures around financing for prospective occupants. Also, it appears these managers are in possession of new data or at least acting on demand-driven data to style existing residential spaces to match the economics of the mass market. Concepts such as ‘shared spaces’ and ‘short-lets’ seem to be an increasing favorite for occupants and property managers alike, showing a change in attitudes.

Disclaimer

Comments expressed here do not reflect the opinions of Vanguard newspapers or any employee thereof.