. expected to hit 80% by year end.

By Dele Sobowale

VANGUARD, November 10, 2025.

“Where is the money?” Weekend Trust, November 8,9, 2025.

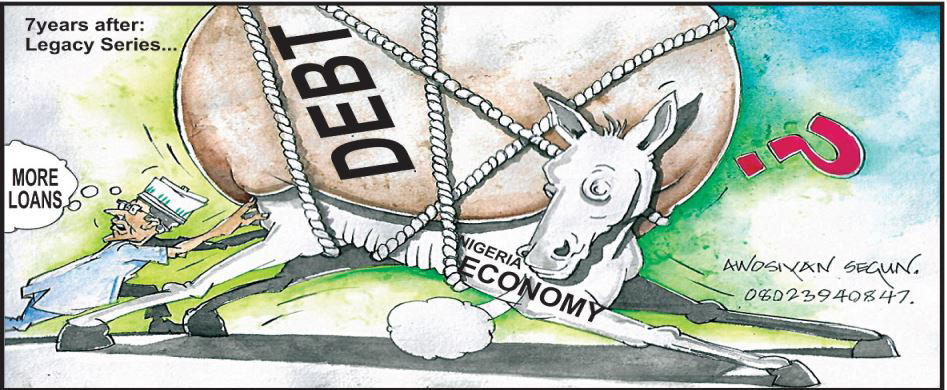

Drowning in debt and liking it

As a subscriber to several newspapers, it has been possible to follow virtually all the issues affecting our lives from several perspectives. Every Monday brings a big harvest of papers. Since charity begins at home, VANGUARD is read first. Then, I move to Weekend and Daily Trust. Last week, the two papers served headlines which should be deeply concerning to every Nigerian – including President Bola Tinubu. That the Federal Government exceeded the borrowing estimate in the approved 2025 budget was not surprising as I will presently establish. It was the magnitude of the negative variance that was seriously alarming.

Just as that alarm bell was ringing in my head, Afeez Hanafi and Abdullateef Aliyu, on page 4 of the Weekend Trust, asked the question: “Where is the money?” They then proceeded to present four pages of analysis to raise the fundamental issues about accountability and the impact of governments’ economic policies. Reading the four pages carefully, it is difficult to escape the impression that the benefits of fuel subsidy removal and the deeper currency devaluation are either being hoarded by a lucky few or are being, once again, dissipated on projects and programmes which add no economic value to the lives of Nigerians.

NIGERIANS FOREWARNED

Nigerian leaders at federal and state levels, with very few exceptions, are always short-sighted. The focus is always the next election. So far, no President would go down in history as Mandela did – who spent one term and voluntarily left office. The followers and appointees are just as myopic. They forget that the leader they follow might not be in power forever. They excuse atrocious economic policies, while in government, join in condemning his successors doing the same thing.

Below is an article published in the first quarter of last year to draw attention to the intractable fiscal irresponsibility of our Presidents and Governors.

“BORROWING IS THE OPIUM OF NIGERIAN GOVERNMENTS.

“The DMO said as of March 31, 2024, the country’s domestic and external debts stood at N121.67 trillion ($91.46 billion). Nigeria’s debt rose by N24.33 trillion within three months – from N97.34 trillion ($108.23 billion) in December 2023 to N121.67 trillion ($91.46 billion).” Channels Television.

Nigerian government leaders, Presidents and Governors, are addicted to loans the same way drug addicts cannot kick the habit; and become increasingly hooked. What Dr Ngozi Okonjo-Iweala persuaded Obasanjo to do in 2004, that is to pay off Nigeria’s external loans was so alien to our government leaders that one late former Governor called her “stupid”. Since then, no President or Governor has repeated it – even when opportunities made it possible. The years 2010 to 2013 were Nigeria’s second golden years since the oil boom of the 1970s. Despite the monumental waste, Nigeria went from 1973 to 1978 without borrowing a cent. Instead, the country ran positive balances of trade. We were lending not borrowing. Many horrible things started with Obasanjo – borrowing instead of looking inwards was one of them. The $2.8 billion loan he took as Military Head of State (with assurances that the debt would be easily repaid) started the ball rolling until the debt load reached $36 billion; and Nigeria was seeking debt relief. Since then, borrowing has become such an unshakable habit that when crude prices averaged $110 per barrel under Yar’Adua/Jonathan, instead of saving more for the rainy day and borrowing less, the President and all the Governors went on a borrowing binge. Till today, it has been difficult to understand what the Ministers and Commissioners of Finance were telling their principals.

What is clear from records available everywhere was the notion that reducing the FG’s or states outstanding debts was out of the question.”

Since that article, the situation had gone from bad to worse. By the time Jonathan left office in 2015, only the future of our children had been mortgaged by the FG. Buhari added our grandchildren to the list of perpetual debtors. At the rate the FG is acquiring more debts, our great grandchildren would have been drawn into the debt trap. The first question now is: when will this dangerous trend stop? The second is: who will stop it? The third is: how will it stop? Surprisingly, the answers to the first and second questions are indefinite. The third is more obvious given recent events globally.

It is one of the verdicts of economic history that allowing an unsustainable policy to continue unchecked results ultimately in a situation in which there are no good options left. Nobody can accurately predict when the crunch would come. Almost invariably, those responsible for the economic problems created are never able to solve them. Leaders who operate on the “borrow and spend principle” are like addicts believing that another intake would solve their problems. They will continue to borrow as long as there are lenders willing to provide the funds. And, they will accept virtually any conditions imposed. Eventually, the end comes in two ways – the International Monetary Fund, IMF, steps in to impose conditions which invariably imposes more hardships on the people than ever before.

Argentina and Nigeria present case studies in these regards. Recently, the US stepped in to offer bail-out to Argentina when all other sources dried up. Since it is axiomatic that he who pays the piper dictates the tunes, the South American country has surrendered some of its sovereignty for money.

The Nigerian government recently launched a $2.35bn Eurobond in several countries, which was oversubscribed by 400 per cent. FG’s spin doctors attributed the result to confidence in the Nigerian economy. Nothing can be further from the truth. The bonds were oversubscribed because the interest rates are 9.25 per cent and 10.375 per annum for 6.5 years and 10 years bonds respectively in markets where interest rates are 6 per cent or less per annum. Nigeria, a relatively poor country is paying almost 100 per cent more than Singapore to borrow the same amount of money. Most of the investors are probably high net worth individuals seeking a tax dodge and staking, what to them is chicken change, to reap above average returns. At any rate, Nigeria still needs to repay capital plus shylock interests – over a period of six to 10 years – long after Tinubu must have left office.

When will it end? Given the Tinubu government’s appetite for loans, it is obvious that the FG cannot on its own stop borrowing more; and the National Assembly is not ready to follow America’s example and put a stop to it. The IMF or US might step in to do what we have failed to do ourselves one day.

Where is the money? That remains the one trillion naira question.

Follow me on Facebook @ J Israel Biola.

Disclaimer

Comments expressed here do not reflect the opinions of Vanguard newspapers or any employee thereof.