…DMO flags off Q3’19 bond programme with N145bn

By Babajide Komolafe

ANALYSTS are divided in their predictions for the outcome of the Monetary Policy Committee (MPC) meeting holding today and tomorrow even as the Debt Management Office (DMO) flags off its bond issuance programme for the third quarter (Q3’19) with a N145 bond auction this week.

At the end of its meeting in May, the MPC retained all its benchmark indices with the Monetary Policy Rate remaining at 13.5 percent, the Cash Reserve Ratio (CRR) at 22.5 percent and Liquidity ratio at 30 percent. This was contrary to the 50 basis points cut in the MPR, to 13.5 percent from 14 percent, announced at the end of the previous MPC meeting held in March.

Nigeria external reserves stand at $45bn as at June – CBN(Opens in a new browser tab)

While most analysts project that the MPC will maintain the status quo as it did at the end of the May meeting, analysts at FSDH Merchant Bank, however, differed, projecting that the MPC will reduce the MPR further by 50 bpts to 13 percent.

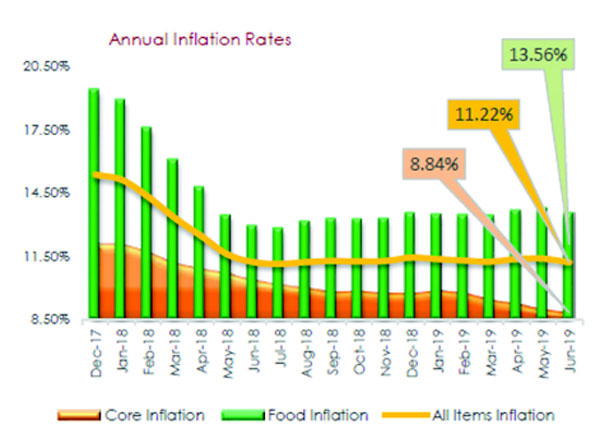

According to the FSDH analysts, “An increase in policy rates is not an option under the current economic situation in the country. The short-term outlook of the inflation rate (which points to a declining trend, other things being equal), stability in the foreign exchange rate, and the drive of the Federal Government of Nigeria (FGN) and the CBN to stimulate growth in the economy all support a rate cut. Such a cut would add weight to the implementation of the CBN’s five-year strategic plan.

“FSDH Research anticipates a 50 basis points reduction in the Monetary Policy Rate (MPR), as well as a possible adjustment to the asymmetric rates around the MPR.

“While FSDH Research notes there are a number of structural challenges in the economy at the moment that can reduce the effectiveness of monetary policy, there are strong indications that the MPC members may vote to reduce the MPR to 13 percent. The market should not be surprised if the MPC also announces a reduction in the rate of the Standing Deposit Facility (SDF) of the banks with the CBN. It is possible that the MPC will maintain the Liquidity Ratio and CRR at the current level.”

Analysts at Lagos based Afrinvest however said: “Based on our analysis of recent issues, we believe the MPC would maintain status quo on all policy rates in the next meeting – (MPR) at 13.5 percent, Cash Reserve Ratio (CRR) at 22.5 percent, Liquidity Ratio at 30.0 percent and asymmetric corridor at +200 and -500bps around the MPR. We note that monetary easing is already on course in the debt market as the MPR is only symbolic. We expect the CBN to continue to ease by guiding yields downward through its less aggressive liquidity management operations.

“Recently, we have observed a decline in the frequency of Open Market Operations (OMO) sales by the CBN as 14 OMO sales were held in January relative to two sold in June 2019.

“With a focus on exchange rate as the key monetary policy anchor, we believe downside risks are limited due to a strong external reserves balance, rising oil prices, improving oil production and monetary easing by systemically important central banks. We rule out the possibility of an interest rate hike as risks to inflation remain moderate and concentrated on the supply side.”

Making a similar projection, analysts at Lagos based Cowry Assets Management Limited said: “We expect the MPC to retain the MPR at 13.50 percent, within the existing asymmetric corridor of +2 percent and -5 percent in line with its current drive for economic growth.”

Analysts at Lagos based Financial Derivatives Company Limited also projected that the MPC will maintain the status quo saying, “The moderation in the inflation numbers will be cheery news to the doves in the monetary policy committee at their meeting next week. However, given the tepid economic growth, we expect the committee to continue with its wait and see approach on monetary policy parameters and continue to use OMO activities and forex interventions to control liquidity in the system.”

DMO to auction N145bn FGN bond

Meanwhile the Debt Management Office (DMO) will this week flag off its debt issuance calendar for Q3’19 with a N145 billion bond auction. Last week, the DMO announced plans to offer between N360 billion and N480 billion worth of 5, 10 and 30-year bonds. This represents N120 billion above its offer in Q2’19 when it offered between N255 billion and N345 billion.

The N145 billion to be offered this week comprises N40 billion of five-year bonds, N50 billion worth of 10-year bonds and N55 billion worth of 30-year bond.

Analysts expect oversubscription for the bonds in view of the huge excess liquidity in the interbank money market, and hence lower stop rates on the bonds. Speaking in this regard, analysts at Cowry Assets Management Limited said: “We expect the bonds to be issued at lower stop rates amid sustained demand pressure on fixed income assets.”

Disclaimer

Comments expressed here do not reflect the opinions of Vanguard newspapers or any employee thereof.